Fund might be a daunting and you will frightening element of existence, but with such jargon combined with salespeople desperate for the dollars, how do you discover what’s going on otherwise off? Here we are going to define just what a keen SBA eight(A) financing is, exactly what an enthusiastic assumable loan was and you can if SBA 7(A)is why can be considered assumable.

SBA signifies Small company Administration. Home business Government is a beneficial U . s . authorities agencies that provides out loans to small enterprises and you can business owners to help them expand or simply start her providers.

New eight(A) is one of the applications and therefore SBA uses, therefore works well with individuals who must get genuine home eg office bed room otherwise buildings. Many people utilize it purchasing organization devices including day spa chair and color offers, nonetheless it may also be used to re-finance latest company obligations.

Refinancing occurs when you only pay from your debt with individuals more courtesy an alternate mortgage. The latest financing would be to reduce your interest.

To be eligible for that it loan, you should be a small business one operates having profit, you are not a charity. You have to do company in america. You really need to reveal that you have got used your very own assets before getting to this point, definition you really have marketed your car or truck or reduced the coupons membership.

You need to determine the reasons why you you want that loan and that the business would-be successful for this. And finally, you can’t have most other debts with the You.S regulators.

The attention with the SBA eight(A) finance was consistent, which means your monthly obligations won’t change. This would move you to available to your repayments.

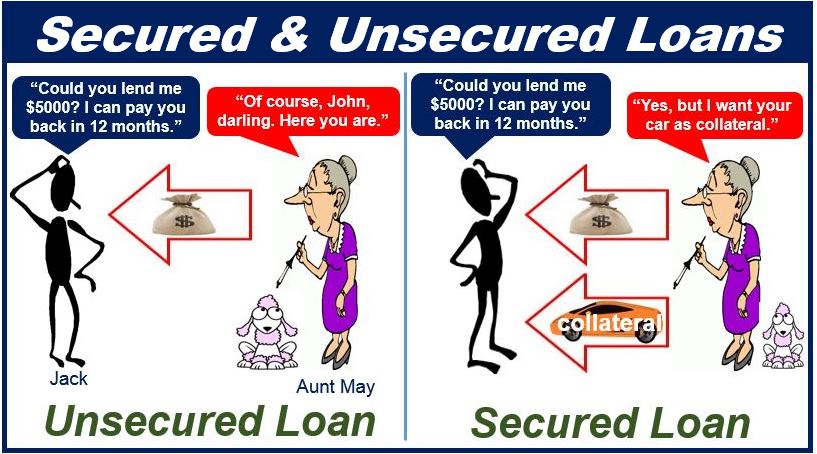

An assumable financing try that loan that can be bought from the a good consumer. The latest purchaser would and then make money into financing with the same appeal price and same length of time left because of the brand spanking new owner.

If you utilize the borrowed funds to pay for the house, particularly a mortgage, then buyer do own your house and certainly will pay off the mortgage in one low rate that you are currently paying and with the exact same amount of time you had left the fresh obligations in the.

Not totally all fund could be presumed, and there’s just a bit of history around why. During the early 1980s, very mortgages was assumable for as long as new buy repaid a charge. This was no issue up until the financial drama hit and rates arrive at feel high.

Originally mortgage loans had been as little as 6 or seven %, however with this attract growth, the brand new commission expanded in order to 20.

That it meant one people don’t need the brand new mortgage loans anymore just like the 20% attract are too much. Rather, it arrive at get assumable loan mortgage loans to keep a similar 7% as earlier in the day customers.

However, this is a good way for new people to track down to the fresh new hike inside repayments, nevertheless finance companies have been lacking money. Banking companies began to crash and you may necessary government bailouts to remain afloat. This was charging the government and also the finance companies money.

Another term try introduced to the majority loans named Owed at discount. That it term meant that when a home is actually sold, the borrowed funds mortgage is because of be distributed to the income time, therefore ending the brand new purchases of remaining the lower interest given that they will need to get a completely new mortgage.

Of several claims (added from the California) debated this term ran up against user rights, but not, the federal government try shedding so much money which they allow condition feel lead in any event.

At this time, assumable funds try unusual, while a purchaser planned to pick an enthusiastic assumable financing, they will need fulfill a lot of the bank’s standards before any discussions have been made.

So, whatsoever that, are SBA eight(A) funds assumable? The answer is sure. Although not, even though it is you are able to to offer your organization from this approach, the procedure is complex.

The first thing you will need to reason behind is the brand-new SBA qualification recommendations. The fresh new debtor will need to violation which qualifications take to only as you did. Nonetheless they must have enough financial strength and you will team experience to help you convince SBA one to defaulting was impractical.

As opposed to your totally new qualification recommendations, you will find a few a great deal more criteria that the brand new borrower tend to have to match. The new instructions must be the primary people who own the organization, plus they need to have both the same number of feel as you or higher experience.

Its credit rating need to be A good, and thus it prices in the 680 or even more. This new business person might also want to have the ability to tell you monetary electricity to repay the whole mortgage; capable do this due to a collateral items such as https://paydayloansconnecticut.com/woodbury-center/ for example other household worth the same amount of money and therefore can not be offered throughout the assumption techniques.

Ultimately, such this new agreements will receive an excellent Due on sale otherwise Passing clause attached to these to avoid the loan away from becoming assumed having a second go out.